Full year 2012 Results

Press Release

Haaksbergen, the Netherlands

6 Mar 2013

Strong operating result in fourth quarter

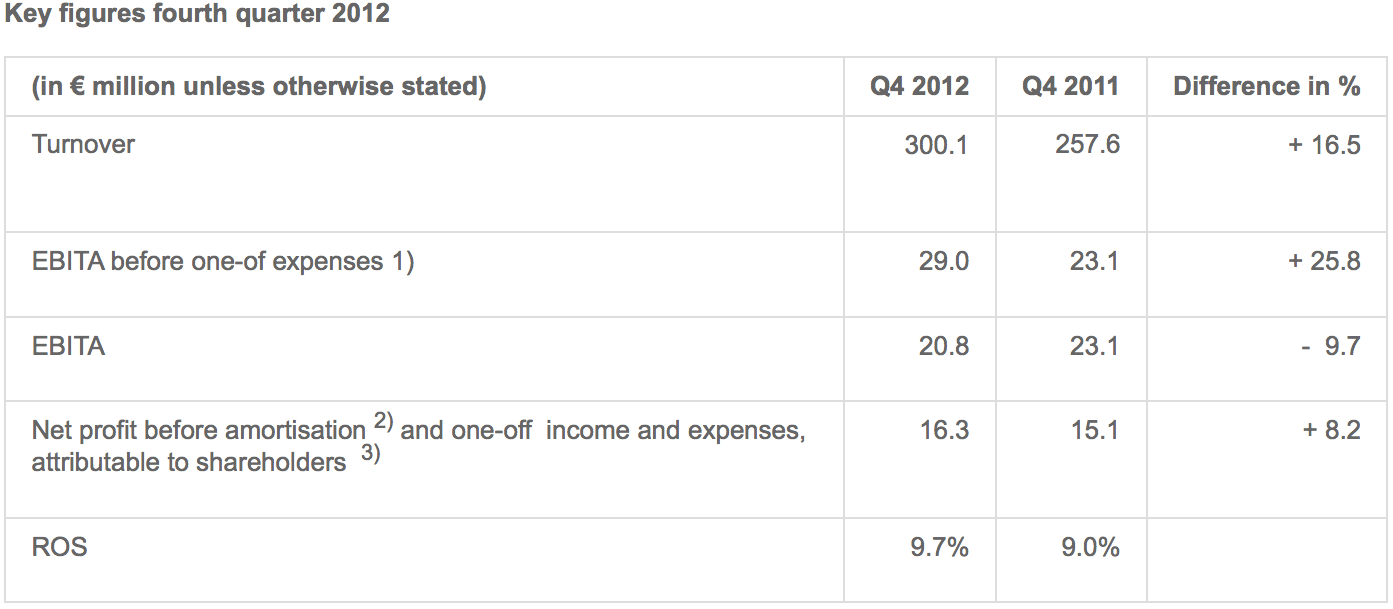

Highlights Q4

- Turnover up 16.5%, organic growth 2.0%.

- EBITA rises 25.8% before one-off expenses, largely due to strong increase in underlying result at Building Solutions.

- One-off charge of € 11.3 million for efficiency programme Building Solutions.

- Improvement in market conditions in industrial sector.

- Challenging market conditions in Building Solutions.

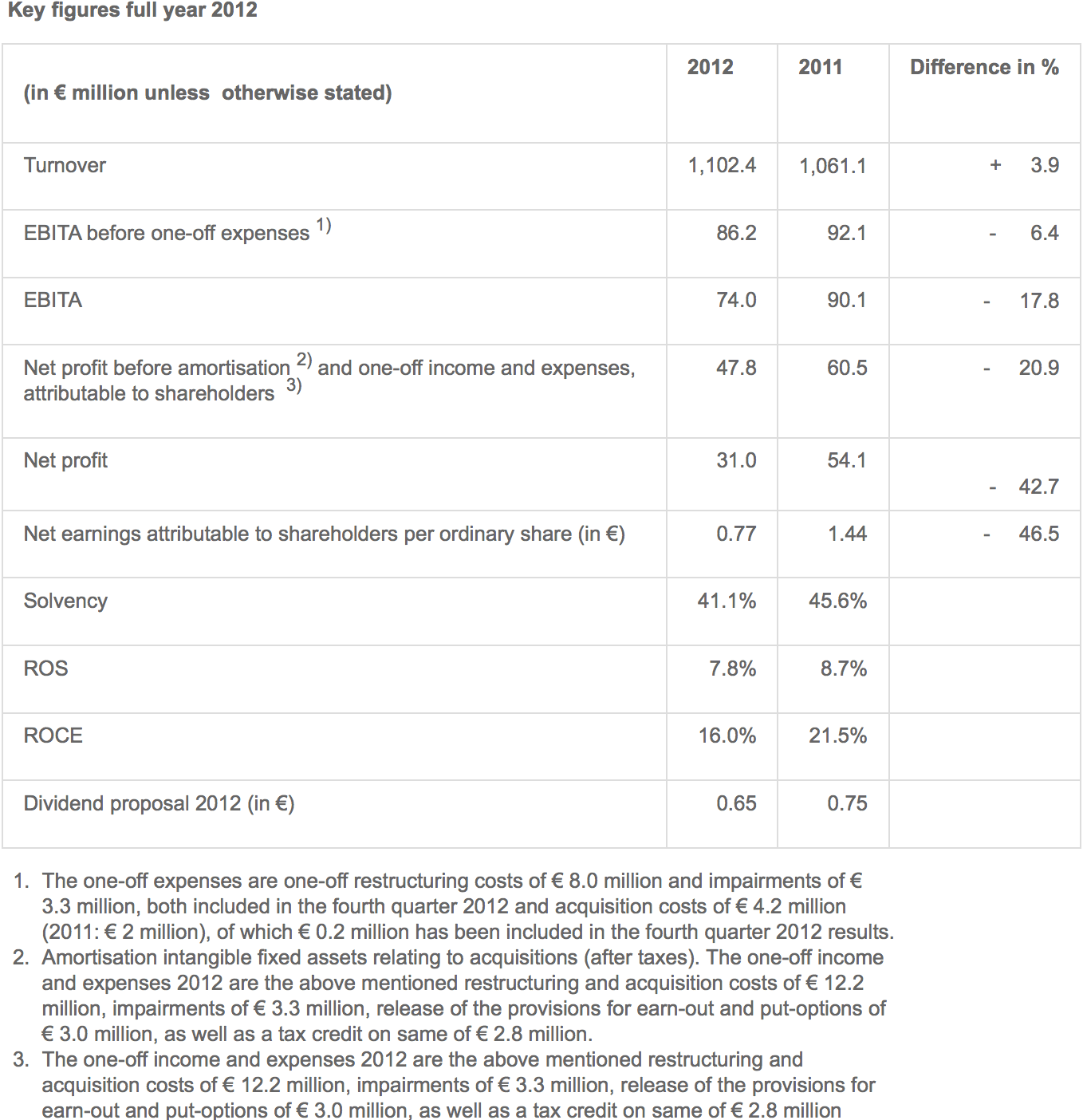

Highlights 2012

- Turnover up slightly at € 1.1 billion, organic decline of 5.0%.

- Drop in EBITA due to Industrial Solutions segment.

- Net profit before amortisation and one-off income and expenses in line with expectations.

- Successful expansion vision & security segment via acquisition of Aasset Security and Augusta Technologie.

- Dividend proposal € 0.65 per (depository receipt for an) ordinary share.

Alexander van der Lof, CEO of technology firm TKH:

“The year 2012 was dominated by challenging market conditions in the building and construction sector and a certain degree of reluctance to invest in the industrial sector. However, with a ROS of 9.7%, the fourth quarter showed that thanks to its strong strategy TKH can realise solid results even in difficult conditions. TKH made considerable progress in 2012 in bolstering its foundations in the field of technology and will continue to do so in the years to come.”

Financial developments

In 2012, turnover was up € 41.3 million (3.9%) at € 1,102.4 million, from € 1,061.1 million in 2011. Acquisitions lifted turnover by 9.1%. Reduced raw material prices had a negative impact of 0.2% on turnover. On balance, turnover fell by 5.0% organically.

Building Solutions showed the strongest increase in turnover, booking a rise of 14.3%. Turnover in Telecom Solutions was up by 3.3%. However, Industrial Solutions recorded a decline of 3.8%. For the full-year 2012, Industrial Solutions accounted for 45% of turnover, down from 49% in 2011, while the share from Building Solutions increased to 40%, from 36%. Telecom Solutions accounted for 15% of turnover, unchanged from the previous year. Innovations once again made a strong contribution to turnover, accounting for 21.2%, compared with 22.8% in 2011.

The gross margin was up in 2012 at 40.9%, from 38.9% in 2011. Operating costs excluding one-off expenses, as a percentage of turnover, rose to 33.1% in 2012, from 30.2% in 2011. When acquisitions are also excluded, operating costs in 2012 were at a comparable level to 2011. While the cost level was higher in the first half of 2012 compared with the same period 2011, we brought this more into line with market conditions in the second half. Depreciations came in at € 17.5 million, above the € 15.3 million booked in 2011, due to the higher level of investments in 2011 and 2012.

The operating result before amortisation of intangible assets and one-off income and expenses fell by 6.4% to € 86.2 million in 2012, from € 92.1 million in 2011. The EBITA in Telecom Solutions was up 13.5% compared with 2011. At Building Solutions, EBITA rose by 11.9% mainly due to acquisitions. EBITA at Industrial Solutions was 13.8% lower than in the previous year, primarily due to lower order intake in 2011 and in the first half of 2012. The ROS for TKH Group as a whole dropped to 7.8% in 2012, from 8.7% in 2011.

In 2012, an amount of € 4.2 million was spent in relation to acquisition costs, largely for the acquisition of the majority stake in Augusta Technologie (2011: € 2.0 million for the acquisition of Siqura). The one-off expenses for the implementation of efficiency programmes came in at € 8.0 million in 2012 and are included in the costs. In 2012, in the context of these programmes, we also included an impairment of € 3.3 million in the fourth quarter, largely related to loss-making activities in Building Solutions, which will be discontinued and/or divested.

The operating result including these one-off expenses fell by € 16.1 million or 17.8% to € 74.0 million.

Amortisation charges were up € 7.8 million at € 20,9 million, from € 13.1 million in 2011, largely due to the acquisition of KLS Netherlands (2011), Aasset Security and Augusta Technologie.

Financing costs increased to €12.1 million in 2012, from € 7.4 million in 2011. This increase was primarily due to a higher outstanding interest-bearing debt and a negative currency exchange rate effect of € 0.7 million compared to 2011.

The 2012 results include a exceptional gain of € 3.0 million from the release of a provision for earn-out and put-options held by minority shareholders.

The tax burden rose to 23.9% in 2012, from 22.3% in 2011, largely because 2011 included a one-off benefit on previous years from the application of the Dutch innovation tax facility.

Net profit before amortisation and one-off income and expenses, attributable to shareholders came in at € 47.8 million in 2012, down 20.9% from the € 60.5 million reported in 2011. Net profit in 2012 was € 31.0 million, down from € 54.1 million in 2011. Earnings per share before amortisation and one-off income and expenses came in at € 1.28, compared with € 1.63 in 2011. Ordinary earnings per share were € 0.77, from € 1.44 in 2011.

Cash flow from operating activities increased to € 75.2 million, from € 47.4 million in 2011. In 2012, operating capital as a percentage of turnover was 13.1%, up from 11.6% in 2011, largely due to acquisitions.

TKH made net investments in tangible and intangible assets of € 25.7 million in 2012, compared with € 21.9 million in 2011. A large proportion of these related to investments in production locations. TKH also invested € 96.1 million net in acquisitions and participations and € 14.1 million in intangible fixed assets, mainly R&D, patents and licences, which compares to € 7.7 million in 2011. Net bank debt had increased to € 188.2 million at year-end 2012, up € 94.4 million from year-end 2011. The solvency ratio dropped to 41.1% in 2012, from 45.6% in 2011. TKH operates well within the financial ratios agreed with its banks. The net debt/EBITDA ratio was 1.6 and the interest coverage ratio was 9.8.

TKH employed a total staff of 4,736 FTEs at year-end 2012, compared with 4,062 a year-earlier. The increase in the number of employees was almost entirely due to acquisitions.

Progress in realisation of targets and execution of strategy

TKH Group once again devoted considerable attention to its strategic targets and the realisation thereof. Key milestones were the strengthening of our position in vision technology following the acquisition of a majority stake in Augusta Technologie, plus the realisation of our target to book at least 20% of the TKH annual turnover in vision and security systems. These milestones have created opportunities for new growth in selected vertical markets in which TKH can excel thanks to its high-grade technology and added value in the form of services and total solutions. TKH decided to change the name of the ‘security systems’ segment to ‘vision & security systems’, partly in view of the strong increase in the share of turnover from vision technology in this segment.

TKH believes there is still room for improvement in the ROS through a shift in the business mix and the positioning of parts of the portfolio in market segments where we can provide greater added value. TKH once again made substantial investments in technology and R&D capacity to ensure that we are able to build on and increase our technological lead. This could in turn lead to new market positions and growth in market share. The ROS dropped to 7.8% in 2012, from 8.7% in 2011, largely due to the high cost level combined with the surplus production capacity in the first half, plus investments in the organisation. The improvement in the ROS in the fourth quarter to 9.7% supports the ambition for further growth. It should be noted that TKH’s ROS is always strongest in the fourth quarter.

The strong contribution of 21.2% innovations to 2012 turnover, compared with 22.8% in 2011, once again underlines the success of TKH Group.

Developments per solutions segment

Telecom Solutions

Profile

Telecom Solutions develops, produces and delivers systems for applications from basic outdoor infrastructure for telecom and CATV networks to indoor home networking. The focus is on providing customers with care-free systems due to the system guarantees we provide. Around 40% of the portfolio consists of optical fibre and copper cable for node-to-node connections. The remaining 60%, consisting of components and systems in the field of connectivity and peripheral equipment, is used mainly in the network’s nodes.

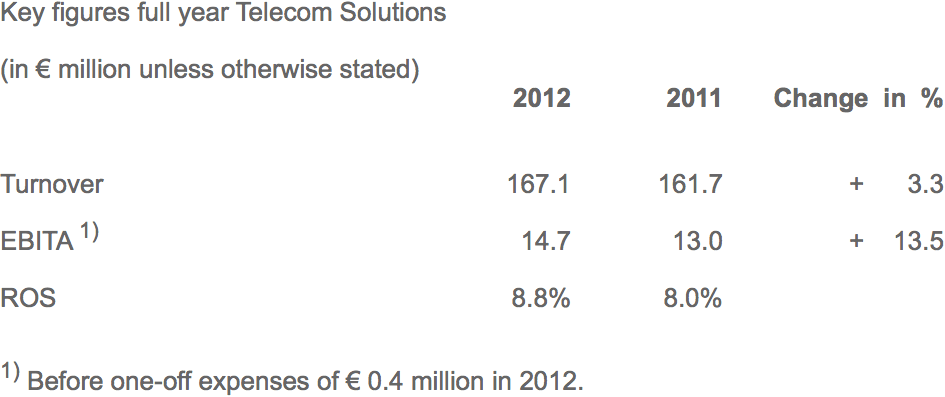

Turnover within the Telecom Solutions segment rose by 3.3% to € 167.1 million. This organic increase in turnover came from the segments fibre network systems and indoor telecom systems. The copper network systems segment recorded a decline in turnover.

EBITA rose by 13.5% to € 14.7 million. This increase was due to volume growth and a related improvement in the margin on the back of higher productivity and cost efficiency. This raised the ROS to 8.8% in 2012, from 8.0% in 2011.

Indoor telecom systems - home networking-systems, broadband connectivity, IPTV-software solutions – turnover share 4.6%

Turnover increased by 9.6%, with the biggest rise in turnover booked in the second half of the year, as a result of the recovering market and a greater proportion of IPTV projects. Demand for multimedia systems and upgrades to home networks increased despite pressure on consumer spending, partly because of the increased penetration of fibre networks.

Fibre network systems – fibre optic, fibre optic cable, connectivity systems and components, active equipment – turnover share 7.6%

Turnover in this segment was up 11.6%. In particular, Germany and Eastern Europe saw turnover growth, as existing network upgrades and the further penetration of fibre networks became a higher priority. The market demand for fibre in Western Europe increased in volume (kilometres of optical fibre) by 6%. The financing of new networks was not an obstacle, although a number of telecom companies took a more cautious stance on the role-out of fibre networks due to high investments in new 4G networks.

The production capacity expansion in China was successful. We were able to utilise the new production facilities from the second quarter onwards and by the fourth quarter capacity had been doubled year-on-year, to annual production of more than 4.5 million kilometres of optical fibre. The new production technology has led to a major increase in efficiency in terms of material use and production rate. Thanks to this, the margin in this segment has improved, despite increased pressure on prices. We strengthened our position in France and made preparations to take advantage of growth in this market by setting up a local entity.

Copper network systems – copper cable, connectivity systems and components, active equipment – turnover share 3.0%

Turnover in this segment dropped 19.2%. After a short-lived upturn in 2011 due to a backlog in network maintenance, market demand declined considerably in 2012. The continued shift of priority to fibre networks and the investments by telecom operators in 4G networks are accelerating the decline in investments in this segment. Margins were down as a result of the drop in turnover but remained positive on the back of effective cost controls.

Building Solutions

Profile

Building Solutions develops, produces and delivers solutions in the field of efficient electro technical technology ranging from applications within buildings to technical systems which, linked to software, provide efficiency solutions for the care and security sectors. The know-how focuses on vision technology and connectivity systems combined with efficiency solutions to reduce the throughput-time for the realization of installations within buildings. In addition, the segment focuses on intelligent video, intercom and access monitoring systems for a number of specific sectors, including elderly care, parking and security for buildings and work sites.

Turnover in the Building Solutions segment was up 14.3%, with acquisitions accounting for 18.7% of turnover growth. Organic turnover was down 4.0%. Lower raw material prices had a negative impact of 0.3%. Organic turnover in the fourth quarter fell 9.0% due to the continued deterioration in the building and construction sector, especially in Europe, and a reduction in inventories. In the course of 2012, we anticipated a continued decline in the building and construction markets and took measures to reduce costs and launched an efficiency programme.

The EBITA before one-off income and expenses increased to € 22.9 million. The vision technology activities of Augusta Technologie made a considerable contribution of € 8.8 million. The efficiency measures we took and the better match between capacity and market demand improved the result on sales considerably. In the fourth quarter, the ROS came in at 7.9%, excluding the contribution from Augusta Technologie (Q4 2011: 5.6%). In particular the results from the segments connectivity and security showed an improvement, whereby in the fourth quarter, the market conditions for the connectivity segment were particularly challenging. The ROS for the full year fell slightly to 5.3% from 5.4% a year earlier.

Building technologies – energy-saving light and light switch systems, energy management systems, care systems, structured cabling systems – turnover share 8.4%

Turnover in Building Technologies was up 11.1%, with 3.6% of this from acquisitions. There was a considerable increase in the contribution from care systems for both intramural and extramural care. The market for remote healthcare seems to be increasingly open to new technologies that facilitate better and more efficient health care. TKH technologies are an effective response to this demand. The increased demand for healthcare systems compensated for the drop in demand in the building and construction sector. Efficiency solutions in the field of energy-saving lighting systems and intelligent parking systems also outperformed the market.

Vision & Security systems – Vision technology, systems for CCTV, video/audio analysis and detection, intercom, access control and registration, central control room integration – turnover share 16.0%

Turnover in this segment was up 47.0%. The increase was due to the acquisitions of Aasset Security and Augusta Technologie. Organic turnover was down 10%. The market conditions in the building and construction sector and the reduction in public sector investments had a strongly negative impact on growth. Thanks to expansion outside the Netherlands and the increasing demand for TKH’s efficient technological solutions, we were able to counteract to some extent the impact of the deteriorating market conditions. TKH’s leading position in vision technology plays a key role in this. The growing need to replace the human eye with cameras in the field of security, as well as for process and product controls, means that investments in this segment are becoming an ever greater priority. TKH’s positioning in the market for vision and security-related tunnel technologies developed positively.

Connectivity systems – specialty cable (systems) for shipping, rail, infrastructure, solar and wind energy, as well as installation and energy cable for niche markets – turnover share 15.3%

Turnover was down 5.9% due to lower raw material prices (effect of 0.7%) and the reduction of inventories at our production companies. Excluding these effects, turnover was more or less unchanged from the previous year. The market conditions were challenging due to the reduced market volume in the building and construction sector, as well as in the infra and solar market. Measures introduced in the course of 2012 to improve efficiency, strengthen the commercial organisation and increase internationalisation meant that despite the strong decline in demand, billed turnover was more or less unchanged and the result improved in the fourth quarter. We made substantial investments in the development of the portfolio, services and the organisation to boost our market positions in the niches in which TKH is active.

Industrial Solutions

Profile

Industrial Solutions, develops, produces and delivers solutions ranging from specialty cable, plug and play cable systems to integrated systems for the production of car and truck tyres. Its knowledge in the field of automation of production processes and the improvement of the reliability of production systems gives TKH the distinctive ability to respond to the need in a number of specialized industrial sectors, such as tyre manufacturing, robotics, medical and machine construction industries, to increasingly outsource the construction of production systems or modules.

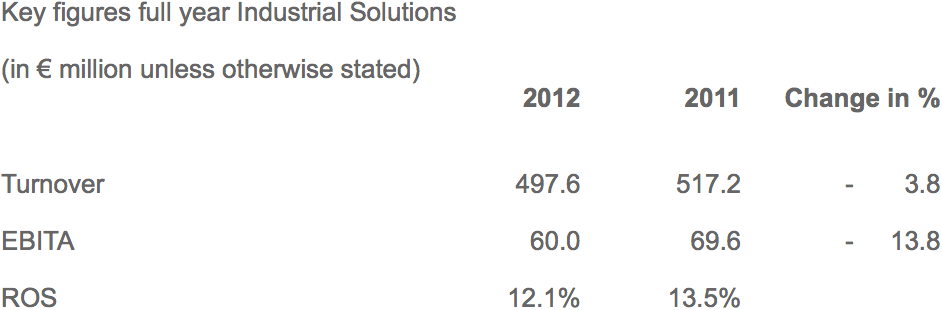

Turnover in the Industrial Solutions segment dropped to € 497.6 million. On average lower raw material prices had a negative impact of 0.3% on turnover. The acquisition Augusta Technologie accounted for 4.8% of turnover. The organic drop in turnover was 8.3%. The decline in turnover was due to a reluctance to invest that has been affecting the market for capital goods since mid-2011.

EBITA dropped to € 60 million. In percentage terms, the decline in EBITA was greater than that in turnover due to a relatively high cost level related to maintaining production capacity for projected medium-term growth. From the third quarter onwards, order intake increased compared to previous quarters. The ROS dropped to 12.1% in 2012, from 13.5% in 2011, but remained at a healthy level.

Connectivity systems – specialty cable systems and modules for the medical, robot, automotive and machine building industries – turnover share 21.7%

Turnover in the connectivity systems segment dropped 3.4%. Lower raw material prices had a negative impact of 0.6% on turnover. The reluctance to invest in the industrial sector had a negative impact on the turnover in the machine construction and automotive sectors. We were able to offset some of the decline in some sectors through further internationalisation and by focusing on innovations for the medical sector and the robotics sector in the form of complete cable systems. The fourth quarter saw organic growth in this segment.

Manufacturing systems – advanced manufacturing systems for the production of car and truck tyres, can washers, product handling systems, machine operating systems and test equipment - turnover share 23.4%

Turnover in manufacturing systems was down by 4.2%. The organic drop in turnover came in at 13.3%, largely due to the low level of investments in the tyre manufacturing industry, as a result of the developments in the automotive sector that date back to mid-2011. The ensuing reduction in order intake translated into reduced turnover for the tyre manufacturing systems segment in 2012. A positive development was the higher order intake realised from the third quarter onwards. This confirms that the previously announced medium-term investment plans in the tyre manufacturing industry are now taking shape. The need for greater efficiency and quality improvements is a good motivator for investments in TKH’s technology, despite less positive developments in the automotive sector. We expanded R&D capacity to increase our technological lead and target an increase in market share.

The remaining segments in manufacturing systems booked an increase in order intake and a rise in turnover.

Dividend proposal

At the General Meeting of Shareholders to be held on 7 May 2013, TKH will propose to pay a dividend of € 0.65 per (depository receipt for a) share for 2012, compared with € 0.75 in 2011. This is equivalent to a pay-out ratio of 50.8% of the net profit before amortisation and one-off income and expenses and 84.4% of net profit. TKH will propose that the dividend be paid out in the form of an optional dividend, in cash or shares, and that it be charged to the reserves, The pay-out of the dividend in shares will be determined one day after the end of the optional period on the basis of the average share price in the last five trading days of said optional period, which will end on 27 May 2013. The dividend will be payable, either in cash or in shares, on 30 May 2013.

Proposed appointments to the Supervisory Board

At the General Meeting of Shareholders of 7 May 2013, Messrs H.J. Hazewinkel and P.P.F.C. Houben will step down as members of the Supervisory Board, in line with the prevailing rotation schedule. Messrs Hazewinkel and Houben are eligible for reappointment and they will be nominated for reappointment during the General Meeting of Shareholders of 7 May 2013.

Proposal for amendment to Dutch large company regime

TKH Group NV currently voluntarily applies the complete Dutch large company regime. In the General Meeting of Shareholders of 2009, TKH pledged that the subject would return to the agenda if, for a consecutive period of two years, the percentage of staff employed in the Netherlands were to fall to or below 45%. The percentage of TKH staff employed in the Netherlands in 2011 and 2012 was below 45%. The company will therefore propose to the General Meeting of Shareholders that the limited large company regime be introduced. We will also propose that the 2013 General Meeting of Shareholders adopt a resolution to amend the articles of association in order to implement the limited large company regime.

Outlook

TKH operates in a number of segments with varying market conditions. It is unclear what impact if any the economic conditions will have in 2013.

In Telecom Solutions, we expect continued growth in investments in optical fibre networks. European plans to roll out FFTH connections have now been clarified and we are in a solid position in the European market to grow in line with market growth. Turnover in copper networks will continue to decline in line with the shift in investments towards optical fibre networks.

In Building Solutions, we expect a continued decline in investment levels in the building and construction sector and a continuation of challenging market conditions. This will impact margins in this segment, which together with lower volumes will have a negative impact on profit. However, a number of market niches have potential for growth. Due to the consolidation of Augusta Technologie for the full year 2013, on balance we expect to realise profit growth in Building Solutions.

In Industrial Solutions, the order intake increased in the second half of 2012 and this is likely to result in an improvement from the second quarter of 2013. However, it is unclear to what extent this growth in order intake will continue in the coming quarters, in view of the difficult conditions in the automotive sector. A further increase in market share, on the back of our strong technological positioning, does offer perspective for growth in the medium-term. At the moment, we expect the 2013 result in this segment to be in line with the 2012 result.

In view of the uncertain economic conditions in a number of segments, it is too early to make a profit forecast for 2013 for TKH as a whole. As usual, we will aim to publish a forecast for the full year 2013 profit at the presentation of the half-year results in August 2013.

The complete press release and the powerpointpresentation can be downloaded in PDF